Update as of April 2026:

Recent judicial developments have temporarily paused the FinCEN real estate reporting requirement. Reporting persons are not currently required to file real estate reports with FinCEN and are not subject to liability if they fail to do so while the order remains in force.

What this means for buyers and sellers:

At this time, real estate transactions can proceed without additional FinCEN reporting requirements. While this rule may be reinstated or revised in the future, there is currently no action required from buyers or sellers related to this reporting.

Original Guidance (Now Temporarily Paused)

Starting March 1, 2026, a new federal rule was set to apply to real estate transactions across the entire country. This rule requires settlement agents, attorneys, and other reporting professionals to share details of certain residential real estate deals with the Financial Crimes Enforcement Network (FinCEN), a division of the U.S. Department of the Treasury that works to prevent financial crimes like money laundering and fraud.

Right now, this requirement only applies to select counties in Colorado, but it was expected to expand statewide—and nationwide—with broader guidelines. The goal is to help reduce scams, fraud, and illegal financial activity in real estate transactions.

Which Transactions Are Affected?

A transaction would need to be reported if all of the following apply:

- It involves residential real estate (such as single-family homes, condos, townhomes, small multi-family properties up to 4 units, mixed-use properties, or vacant land intended for residential use).

- The purchase is made in cash or without a traditional mortgage lender.

- At least one buyer is a legal entity, such as an LLC, corporation, partnership, or trust.

What This Means for You

If your transaction meets these criteria, additional information would typically need to be collected from both the buyer and seller before closing, and the designated reporting party would submit a report to FinCEN.

This report would be filed either:

- By the end of the month after closing, or

- Within 30 days of closing

(whichever comes later).

While these requirements are currently paused, this section reflects how the process is expected to work if and when the rule is reinstated.

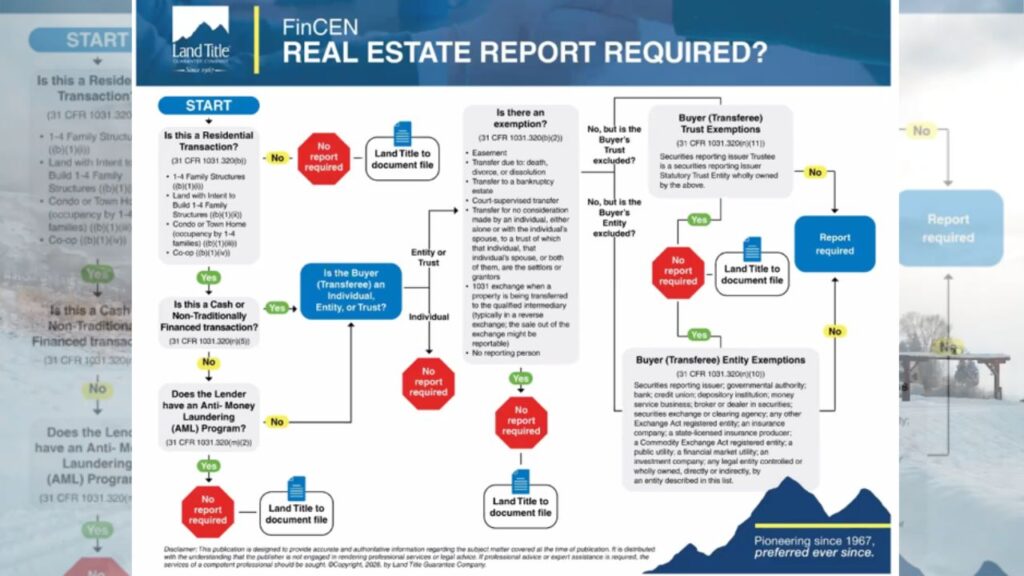

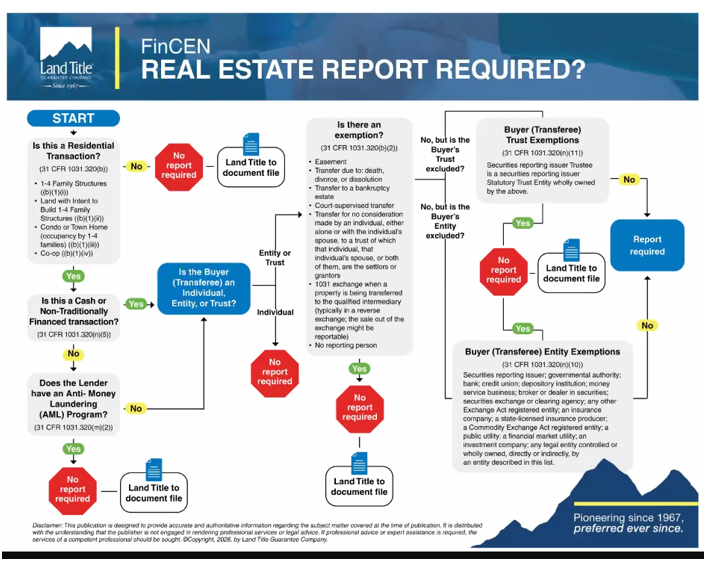

How to Determine if a FinCEN Report is Required

This flowchart walks you step-by-step through whether a real estate transaction needs to be reported to FinCEN. Think of it like a checklist—if you answer “yes” to certain questions, you move forward; if “no,” you may be done.

It starts with a simple question: Is this a residential real estate transaction?

This includes single-family homes, condos, townhomes, co-ops, small multi-family properties (up to 4 units), and certain vacant land intended for residential use. If the answer is no, then no report is required.

Next, ask: Is the purchase being made with cash or non-traditional financing?

If the buyer is using a traditional mortgage lender, the transaction typically does not need to be reported. If it is cash or alternative financing, move to the next step.

Then: Does the lender already have an Anti-Money Laundering (AML) program?

If yes, no report is required. If no, continue.

From there, the flowchart looks at who the buyer is:

- If the buyer is an individual, generally no report is required.

- If the buyer is an entity or trust (like an LLC, corporation, or trust), you move further into the process.

At this point, the flowchart checks for specific exemptions. These include things like transfers due to death, divorce, bankruptcy, gifts, or certain court-ordered transfers. If the transaction qualifies for one of these exemptions, no report is required.

If there are no exemptions, the next step is to determine whether the entity or trust itself qualifies for an exemption (for example, certain regulated businesses, publicly traded companies, or government-related entities).

- If the buyer qualifies for an exemption → no report required

- If not → a FinCEN report is required

Final Outcome

If a transaction meets all the criteria (residential, cash/non-traditional financing, involves a non-exempt entity or trust, and no exemptions apply), then a report must be filed with FinCEN.

If at any point the transaction does not meet the criteria or qualifies for an exemption, then no report is required.

Keep in mind that this rule is currently paused but may be reinstated or revised based on future legal or regulatory updates. Staying informed will be key if you’re planning to buy or sell in the near future.